Job costing in construction tracks four major cost categories for specialty contractors and subcontractors: labor, materials, equipment, and hourly subs. It’s the financial intelligence system for your projects.

Yet, construction cost tracking can fail for a straightforward reason: data quality. Job costing systems work well when the numbers are reliable. When labor data – your largest cost category – gets reconstructed from memory days later, every calculation downstream carries that same variance.

Your construction accounting software can calculate precisely. Your cost codes can be well-organized. Your project budget can be thorough. The system works when labor data arrives accurately. When timesheets get filled out from memory days after the work happened, that variance flows through every report and makes it harder to manage costs effectively.

Specialty contractors often run sophisticated job costing systems while dealing with cost variances that trace back to labor data quality. When labor hours aren’t captured accurately in the field, the project’s financial health picture becomes less reliable.

Job costing does three things: shows you whether you made money on a completed project, identifies which types of work consistently generate margin, and builds a historical database that makes your estimates more accurate on future projects.

Net profit margins in construction typically run 3-7%. Some research shows margins as low as 3.5% in certain regions. One major cost category running off-target can shift a particular project from profitable to unprofitable. When margins are this tight, cost tracking accuracy matters.

Let’s break down how construction job costing actually works for specialty contractors – and why accurate labor data matters more than most construction firms realize.

What Is Construction Job Costing?

Construction job costing is the process of tracking actual costs against estimated costs across all cost categories: labor, materials, equipment, and hourly subcontractors. It’s project-level financial intelligence that helps you track expenses and make informed decisions throughout the project lifecycle.

Here’s how the job costing process works: You bid a construction project based on estimated costs. As the project progresses, you capture actual job expenses. You compare actual to estimated continuously to track progress. When actual exceeds budget, earlier visibility provides more response options.

The real power? Job costing creates a feedback loop that makes you smarter on every future bid.

You estimated 1,200 labor hours for a particular segment of work. Actual was 1,450 hours. Understanding the variance – weather delays, crew composition, scope adjustments, or estimation gaps – helps you improve job costing for similar work. Multiply this across hundreds of projects, and you build a database of actual costs that makes estimating more reliable over time.

The SmartBarrel Angle:

Construction accounting software – CMiC, Foundation, Vista – handles complex cost allocation, burden rates, and variance analysis effectively.

The system requires reliable input data.

When labor hours are inaccurate, the variance flows through subsequent calculations. Cost per unit reflects that variance. Productivity metrics carry it forward. Variance analysis may point toward issues that originate in the data capture process rather than field operations.

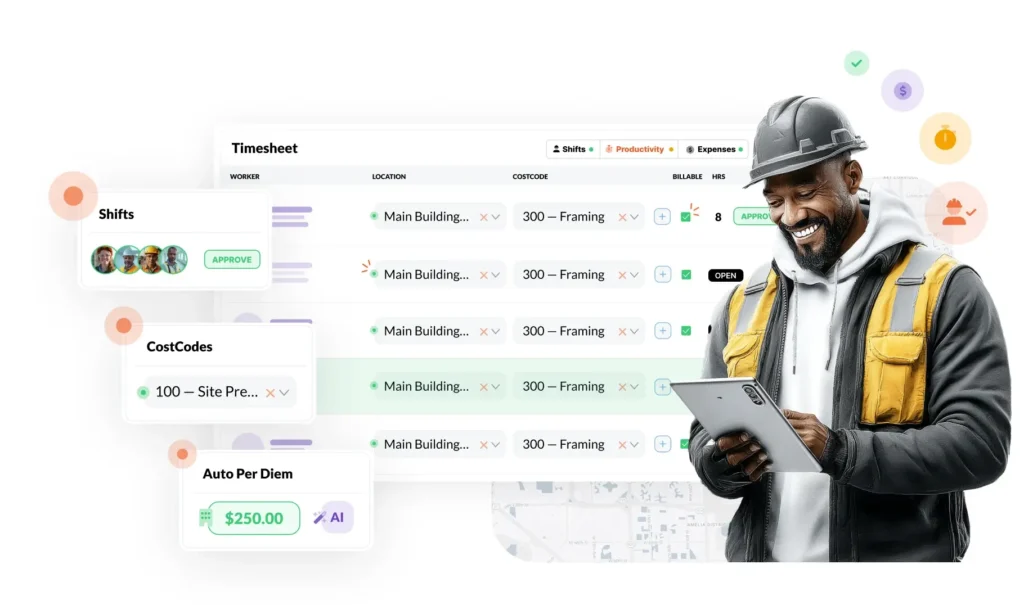

SmartBarrel addresses this by designing labor tracking to prevent errors in the first place. Labor time is captured automatically as work happens, rather than reconstructed later. Foremen review pre-populated, facially verified timesheets instead of building them from memory, and cost codes are assigned during the initial review instead of corrected through multiple passes.

When labor data is captured accurately at the source, job costing systems perform the way they are intended to.

Job Costing vs Process Costing

Process costing tracks costs for standardized, repetitive production. Think manufacturing widgets on an assembly line.

Construction operates differently. Each project represents a distinct scope.

A concrete foundation job in Phoenix operates under different soil conditions, crew composition, weather patterns, and timeline constraints than a foundation job in Minneapolis.

Job costing treats each project as its own cost center. You track costs separately, compare to that project’s specific budget, and analyze that project’s unique variables.

This is why construction uses job costing – process costing approaches don’t accommodate the project-specific variance inherent to construction work.

Different Types of Costs and Their Role in Job Costing

Effective job costing captures four major cost categories. Each behaves differently in construction. Each introduces variance in different ways. Understanding these project costs supports better cost management for any successful construction business.

Labor: The Foundation (40-60% of Project Costs)

Labor typically represents your largest cost category in construction work and presents distinct tracking challenges.

According to industry data, labor represents 20-40% of total project expenses, with commercial construction projects reaching as high as 40-60% when specialized trades are involved.

Labor tracking differs from other cost categories because it requires human-reported data.

Materials arrive with invoices. Equipment costs come with receipts. Subcontractors send bills. Labor requires workers checking in and out, hours being recorded, timesheets flowing to payroll.

This multi-step process can introduce variance: time entries rounded to standard increments, check-outs captured after the fact, cost codes assigned from memory days later. Many construction companies work within these constraints as they manage costs across multiple projects.

SmartBarrel addresses this through biometric facial verification. Workers check themselves in and out. Hours flow to the dashboard as they’re captured. Project managers assign cost codes to pre-populated timesheets rather than creating entries from memory.

The result is labor data captured at the source rather than reconstructed later.

For deeper detail on labor cost calculations, burden rates, and worker classifications, see our complete guide on construction labor cost tracking.

Materials: Price Volatility and Waste (25-35%)

Materials tracking involves several variables:

- Price fluctuations between estimate and purchase

- Waste and breakage on site

- Theft and “shrinkage”

- Storage and handling costs

- Change orders affecting quantities

Your estimate assumed $12,000 in a certain material. Actual POs show $14,200. Price increase? Waste? Scope change? Theft?

Job costing tracks materials cost per unit of work. This reveals waste patterns and informs future estimates.

Equipment: Utilization vs. Standby (5-15%)

Equipment costs include:

- Owned equipment (depreciation, maintenance, repairs)

- Rented equipment (daily/weekly/monthly rates)

- Fuel and operating costs

- Transportation to/from site (including temporary office space setup when needed)

- Idle time between uses

The operational challenge: equipment often sits idle while costs continue. That crane rental? You paid for four weeks. Active use: 12 days.

Job costing reveals equipment utilization rates and supports better resource allocation. When tracking shows a machine sitting idle 60% of the time, you can tighten rental windows or coordinate better across projects.

Subcontractors: Commitment vs. Reality (10-40%)

Subcontractor costs vary by trade and self-perform percentage. A concrete contractor might be 90% self-perform, hiring only rebar or excavation subs. An MEP contractor might self-perform most work but bring in controls or testing & balancing subs.

The tracking challenge: commitment vs. actual.

You’re an electrical contractor who committed $42,000 to low-voltage subs based on their quote. Change orders bring it to $48,500. Actual invoices total $46,200. Which number goes in your job costing report for this particular job? All three – tracked separately.

This applies to any specialty trade you hire: hourly labor subs, equipment operators, niche specialists you don’t carry on staff.

How Categories Interact and Compound Errors

Cost categories interact in ways that affect overall project financial visibility.

Pulling those interactions into a single view is what separates real construction expense tracking from line-by-line bookkeeping, since a labor overrun quietly drags equipment and material costs along with it.

Labor hours influence equipment costs. When a crew runs 15% over estimated hours on a project, equipment costs typically increase as well (additional rental days, more fuel, extended operator time).

Labor hour accuracy affects productivity calculations. Your drywall crew was estimated to install 4,200 square feet in 180 hours. Actual hours were 210. The productivity metric now reflects that variance, which carries forward into your next estimate. Several specialty contractors now reset their field productivity benchmarks at the end of each fiscal year rather than letting incremental variance build up unnoticed.

Material waste often correlates with labor efficiency patterns. When labor hours on a concrete pour aren’t captured accurately, identifying the connection between crew performance and material consumption becomes more difficult.

The compounding effect: Variance in one cost category doesn’t remain isolated to that particular project. It influences the cost intelligence you’re building across all projects and affects your overall financial health.

Key Components of Construction Job Cost Breakdown

Before you can track costs, you need structure. Here’s what makes job costing work.

Cost Code Structure That Makes Sense

Cost codes (also called activities or phases) organize costs within a project.

Your electrical contractor might use:

- 101: Rough-in

- 102: Trim-out

- 103: Low voltage

- 104: Service and panel

Your concrete contractor:

- 201: Footings

- 202: Foundation walls

- 203: Slab on grade

- 204: Elevated slabs

Many contractors use CSI MasterFormat codes as their baseline structure. The CSI code list provides industry-standard divisions and subdivisions.

The design challenge: Too granular, and field crews may not apply codes consistently. Too broad, and you lose visibility into specific cost drivers for future projects.

Direct vs. Indirect Cost Classification

Direct costs tie directly to a specific project:

- Labor hours on that job

- Materials purchased for that job

- Equipment rented for that job

- Subs contracted for that job

Indirect costs support the project but aren’t directly traceable:

- Superintendent time split across multiple jobs

- Shared equipment maintenance

- Project management oversight

- Safety compliance

- Temporary office space and site facilities

The distinction matters because indirect costs require allocation rules for proper resource allocation. How do you split your project manager’s salary across five active jobs?

Overhead Allocation Methods

Overhead (office rent, admin salaries, insurance, utilities) doesn’t tie to any specific job, but jobs need to bear their proportionate share.

Common allocation methods:

- Direct labor hours: Allocate overhead based on percentage of total labor hours

- Direct labor cost: Allocate based on percentage of total labor dollars

- Revenue-based: Allocate based on percentage of total company revenue

The method you choose affects job profitability calculations. A labor-intensive job bears more overhead under hours-based allocation. A high-margin job bears more under revenue-based allocation.

Select a method, apply it consistently, and ensure the team understands what “fully burdened cost” means in your system.

How to Calculate Job Costing in Construction

Job costing in construction isn’t a formula. It’s a continuous process to manage costs throughout the project lifecycle.

1. Capture Costs at the Source

The timing of cost capture affects data reliability and provides real time visibility into the project’s financial health.

Labor: Capture as close to when work occurs as possible. Workers check in/out, hours flow to cost codes. When time entries are created from memory days later, the data carries that delay.

Materials: Capture at PO creation and again at receipt. Track what you ordered, what you paid, and what actually arrived on site – this supports committed cost management.

Equipment: Track usage daily. Log-on/log-off times for owned equipment. Verify rental invoices against actual time on site.

Subcontractors: Track committed costs (contracts), change orders, and invoices separately for each particular project. Maintain visibility into what you’ve committed vs. what you’ve paid vs. what remains.

The SmartBarrel approach: Zero manual entry for labor means data gets captured at the source. The check-in is timestamped, geo-tagged, and facially verified – eliminating the reconstruction step.

2. Organize Costs By Category (Direct/Indirect/Overhead)

Route captured costs to the appropriate categories:

- Direct costs → specific job cost codes

- Indirect costs → allocated based on your chosen method

- Overhead costs → distributed across active projects

Construction accounting software handles this routing when the chart of accounts is configured properly.

3. Compare Actual to Budget and Take Action

This is where job costing systems create operational value and help you track progress effectively.

Run variance reports regularly. Compare actual costs to project budget across all categories:

- Labor: Actual 1,450 hours vs. budget 1,200 hours = 21% over

- Materials: Actual $14,200 vs. budget $12,000 = 18% over

- Equipment: Actual $3,100 vs. budget $2,800 = 11% over

- Subs: Actual $48,000 vs. budget $52,000 = 8% under

The operational step: Investigate variances over 10%. What caused them? Scope change? Productivity variance? Estimation gap? Weather delays?

Document findings. This builds your cost database to improve job costing on future projects.

The timing of variance visibility affects your response options. Real time visibility provides more opportunities to address issues during the active project phase rather than discovering them after completion.

The Benefits of Construction Job Costing

The benefits of job costing deliver value at three levels: individual project performance, overall financial health, and competitive advantage in the construction industry.

Historical Intelligence for Competitive Bidding

Every completed construction job adds data to your estimating database for future projects.

You now know what it actually takes to install 1,000 linear feet of underground conduit in sandy soil with a five-person crew. Not the estimated requirement. The actual requirement.

Next time you’re bidding similar work, your estimate draws from documented performance rather than projection.

Construction firms that maintain detailed job cost records tend to develop more accurate estimates over time. This affects both bid competitiveness and project margins.

Early Warning System for Budget Problems

Job costing provides visibility into cost trends as the particular project progresses and helps you track progress against budget.

You’re three weeks into a six-week construction project. Labor is tracking 15% over budget. Materials are on target. Equipment costs are slightly under.

With this visibility, you can:

- Investigate crew productivity patterns

- Adjust staffing mix

- Increase supervision focus

- Discuss scope adjustments with the client if appropriate

The timing of this visibility affects your response options. Earlier awareness provides more opportunities to address variances during the active project phase.

For real-time cost management approaches beyond job costing, see our guide on construction cost tracking.

Margin Protection on Fixed-Price Work

On fixed-price (lump sum) contracts, cost variance affects your margin directly. Job costing helps monitor this relationship.

According to CFMA data, the average net profit margin in the construction industry runs 3-7%. Some research shows operating margins averaging 10-15%, but net margins typically remain narrow for most construction companies.

A particular job running significantly over budget can offset profit from multiple successful projects and impact overall financial health.

Job costing reveals cost variance as it develops rather than after project completion. This earlier visibility supports better resource allocation and helps you manage costs across multiple projects.

Win T&M Billing Disputes

On Time and Material contracts, you bill the client for actual hours worked and materials used on a specific project.

Clients may question the billing detail. “Were eight workers on site that day? Did they work 10 hours each?”

The quality of your documentation determines the outcome. Timestamped, geo-verified, biometrically verified data provides audit-ready support that addresses client questions directly – protecting the project’s financial health.

SmartBarrel clients report recovering disputed T&M billing because they can provide documentation that addresses GC concerns.

Know Which Work Types Are Actually Profitable

Job costing can reveal margin performance that differs from initial assumptions – essential intelligence for any successful construction business.

Foundation work under 5,000 square feet may show different margins than larger foundations due to mobilization costs representing a larger percentage of total cost on that particular job.

Small T&M service calls may show different margin profiles than estimated when actual costs are tracked systematically.

Job costing reveals which project types, which clients, and which work scopes generate consistent margin. This informs strategic decisions about which work to pursue.

Construction Job Costing Software vs Manual Methods for Construction

Manual job costing presents scalability challenges for construction companies looking to manage costs across multiple projects.

When Manual Job Costing Becomes Limited

Manual job costing means:

- Project managers recording hours on paper timesheets

- Someone transcribing paper to Excel

- Excel formulas calculating labor costs

- Copy-pasting data into separate cost tracking sheets

- Running manual variance reports

- Multiple transcription steps introducing potential variance

This approach can work for a construction business running two small projects simultaneously.

It becomes less viable when you’re running eight construction projects with 200+ workers. The multi-step transcription process introduces variance that compounds through the data and limits cost management effectiveness.

What Integrated Software Actually Solves

Integrated construction job costing systems mean:

- Project expenses captured digitally at the source

- Data flows automatically to construction accounting software

- Real time visibility through variance calculation for each construction job

- Multi-project dashboards to track progress across all jobs simultaneously

- Historical database for estimating future projects and financial planning

- Audit trails for every cost entry to improve job costing

Your accounting software (Vista, Foundation, CMiC, etc.) provides the job costing engine. Your time tracking, procurement, and equipment systems feed it data for the entire job costing process.

The integration requirement:

Your construction job costing systems perform based on the data feeding them.

Construction accounting software with manual time tracking produces job costing reports that reflect the limitations of manual data capture. When labor data – your largest cost category – comes from multi-step transcription, that variance flows through all subsequent calculations and affects your ability to manage costs effectively.

Effective job costing requires accurate data capture at the source, flowing automatically to your job costing software, with minimal manual transcription steps.

SmartBarrel integration: Facially verified time data flows directly to Vista, Procore, Foundation, CMiC. Labor hours get captured at the source rather than reconstructed from memory days later.

Best Practices in Construction Job Costing

Seven practices separate construction firms with effective job costing from those with less reliable systems. These practices support the ability to improve job costing consistently across your organization and contribute to becoming a successful construction business.

1. Design Cost Codes People Will Actually Use

Cost codes become less effective when they’re designed around accounting structure rather than field operations.

Effective cost codes reflect how field crews think about work on actual construction projects. If your electricians naturally break work into “rough-in, trim, panels, and testing,” those divisions work as cost codes. Forcing them into unfamiliar CSI subdivision codes can reduce consistent application.

Test codes with field crews before implementing. If a project manager has difficulty coding a task, consider simplification.

2. Balance the Level of Detail

The cost code structure affects field adoption patterns.

Too many codes can result in inconsistent application, with entries defaulting to catch-all categories. This limits your ability to track expenses accurately.

Too few codes reduce visibility into specific cost drivers across multiple projects.

For most specialty contractors, 8-15 cost codes per construction project represents an effective balance. Complex projects may require more. Simple repeatable work may require fewer for that particular project.

3. Include Indirect Costs

Direct costs are straightforward: labor, materials, equipment costs, subs working on the construction project.

Indirect costs are often not tracked systematically in job costing systems:

- Superintendent time split across multiple projects

- Safety compliance

- Quality control

- Shop fabrication time

- Travel between projects

- Temporary office space and site facilities

Track these expenses for proper resource allocation. Allocate them. Include them in your fully burdened job cost for accurate financial assessment.

4. Allocate Overhead and Executive Time to Projects

Senior leadership and shared support teams often spend time resolving issues on specific projects. That time represents real overhead that affects a project’s true cost.

When this effort isn’t allocated, the project appears more profitable than it actually is, which can distort future planning and bidding decisions.

5. Use Software Systems and Tools

Spreadsheets have limitations for multi-project job costing. Purpose-built construction accounting software and job costing software support more effective cost management.

The value comes from automated variance analysis, historical reporting for financial planning, and integration with estimating. Spreadsheets have limitations when managing multiple projects simultaneously.

But remember: Your job costing software performs based on the labor data feeding it. When timesheets are created from memory days later, even sophisticated software produces reports that reflect that data collection method.

6. Establish and Consistently Implement Change Order Tracking Systems

Change orders create tracking challenges in job costing systems when not separated from the original project budget.

Your original budget was $280,000. Change orders added $45,000. You spent $315,000 actual on that construction job.

Are you 12% over budget? Or are you 3% under budget when change orders are included?

Track original project budget, change orders, and actual separately to track progress accurately. This separation reveals whether cost variance stems from scope changes (client’s responsibility) or productivity variance (your responsibility) – essential to improve job costing on future projects.

7. Understand the Budget

This principle seems obvious but isn’t consistently applied across the construction industry.

Field teams benefit from understanding not just their cost code budget but the context around it for the particular project.

“You’ve got 180 hours budgeted for this phase” provides limited operational context.

“We estimated this phase at 180 hours. You’re at 145 hours through day eight of ten. You’re trending to finish around 165 hours – under budget and ahead of schedule” provides context that supports engagement with the budget process.

Share budget progress. Recognize teams that finish under budget. Investigate variances systematically. Make job cost tracking visible to the people doing the work on construction projects.

Common Construction Job Costing Challenges and How to Improve

Even construction companies with well-designed job costing systems face these recurring challenges. Here’s how to improve job costing by addressing them.

Cost Code Confusion in the Field

The challenge: When workers face too many cost code options, entries may become inconsistent. Project managers spend time correcting codes retroactively, which can affect data reliability.

The approach: Limit active cost codes to what’s currently relevant for that specific project phase. If you’re in the rough-in phase, hide trim-out codes from the selection. Workers choose from five options instead of 30, which supports more consistent code application.

SmartBarrel imports cost codes directly from your ERP or Procore and presents only the codes relevant to the project. The system remembers the cost code a worker was assigned previously and automatically suggests it for the next check-in unless it’s changed. This reduces unnecessary selection steps and supports more consistent, accurate cost tracking.

Split-Time Allocation Across Multiple Projects

The challenge: A superintendent works three hours on one particular project, four hours on another, one hour on a third in a single day. How do you track progress across multiple construction projects accurately?

The approach: Enable workers to check in/out of multiple projects per day. When they move from Project A to Project B, they check out of A and into B.

This works well with mobile time tracking and geo-fencing. When a worker enters Project B’s job site boundary, the system can prompt them to clock into that project.

The Invoice Lag Problem

The challenge: Material invoices arrive two weeks after delivery. Subcontractor bills arrive at month-end. Your job cost report is incomplete because you’re waiting on invoice data.

The approach: Use commitment tracking to manage costs. Log POs when created, not when invoiced. Track committed costs vs. actual costs vs. remaining project budget.

This provides real time visibility into job costs even when invoices lag, which supports effective construction job costing and helps you track progress across multiple projects.

Change Orders Mixed With Original Budget

The challenge: Change order work gets coded to original budget cost codes on a particular job. This makes it difficult to determine whether you’re tracking against the appropriate budget baseline.

The approach: Create separate change order cost codes (CO-01, CO-02, etc.) or use your construction accounting software’s change order management module to track CO work separately.

Separating change order work from original scope in your job costing reports supports clearer project profitability analysis.

Arbitrary Indirect Cost Allocation

The challenge: You’re allocating overhead costs based on a method selected years ago for your job costing systems. The original reasoning may no longer be documented or relevant to current operations.

The approach: Review allocation methods annually to improve job costing. Ask: “Does this method distribute indirect costs appropriately to projects based on how we currently operate?” If not, adjust it.

Document your reasoning. Train your team on what “fully burdened cost” means in your system for consistent cost management.

Fixed Price vs Cost-Plus Contracts and Job Costing Implications

| Contract Type | Payment Structure | Critical Job Costing Needs | Key Risk |

|---|---|---|---|

| Fixed-Price (Lump Sum) | Agreed amount regardless of costs |

| Cost overruns directly cut profit |

| Cost-Plus | Actual costs + markup/fee |

| Client audit rights |

| Time & Material (T&M) | Documented hours + materials |

| Billing disputes |

| Guaranteed Maximum Price (GMP) | Actual costs + fee (capped) |

| Most complex – dual requirements |

Your contract type affects what matters most in the job costing process and the project’s financial health.

Fixed-Price: You Own the Risk

Under fixed-price (lump sum) contracts, the client pays an agreed amount regardless of your actual project costs – making effective job costing critical for project profitability.

What matters most for effective construction job costing:

- Variance from project budget: Cost overruns directly impact your margin and cash flow

- Construction productivity tracking: Labor efficiency affects your financial outcome and overall financial health on the project

- Early visibility: Earlier detection of cost variance provides more response options

Job costing systems that provide regular variance alerts support budget management and help you track progress. Real time visibility into labor data becomes particularly valuable here because labor typically represents your largest variable cost in construction projects.

Cost-Plus: Transparency Is Required

Under cost-plus contracts, the client pays actual project expenses plus a percentage markup or fixed fee.

What matters most for effective cost management:

- Documentation: Clients typically have audit rights for job expenses

- Categorization: The distinction between direct and indirect costs affects reimbursement

- Backup: Each cost requires supporting documentation

Cost tracking quality on cost-plus work affects client relationships and the project’s financial health. When a client questions superintendent time allocation to their project, your documentation needs to support the charge – for example, time spent addressing project-specific change orders.

Audit-ready documentation and detailed tracking of all project expenses supports this contract type.

Time & Material: Proof Is Everything

Under T&M contracts, the client pays for documented hours and materials used on that specific project.

What matters most in job costing:

- Proof of hours worked: Documentation that addresses client questions

- Backup detail: Who worked, what hours, what tasks, what dates

- Timely billing: Billing while work is recent in everyone’s memory

SmartBarrel addresses T&M documentation needs directly. When a GC questions your T&M invoice – “I don’t think you had eight workers there on Tuesday” – you can provide biometric facial verification data showing who was on site, what hours they worked, geo-verified to the job site location.

This level of documentation typically resolves billing disputes and protects project profitability.

Guaranteed Maximum Price: Hybrid Approach

GMP contracts combine cost-plus structure with a ceiling. The client pays actual costs plus fee, but you absorb costs above the guaranteed maximum.

What matters most:

- Everything from cost-plus (transparency, documentation of all job expenses)

- Everything from fixed-price (variance tracking, early visibility into cost trends)

- Clear change order management (changes adjust the GMP ceiling and affect committed costs)

GMP represents the most complex scenario for construction job costing software because you need both audit-ready detail (cost-plus requirements) and variance management (fixed-price requirements) to manage budgets effectively across the project lifecycle – essential for a successful construction business.

Construction Job Costing Calculator

Job costing follows a straightforward formula:

Total Job Cost = Direct Labor + Direct Materials + Direct Equipment + Direct Subcontractors + Indirect Costs + Overhead Allocation

Here’s how this works with real numbers from a mid-sized commercial electrical project:

Direct Costs:

- Labor: $145,000 (1,850 hours × average burdened rate of $78.38/hour)

- Materials: $89,000 (wire, conduit, panels, devices, etc.)

- Equipment: $12,000 (lifts, drills, specialized tools)

- Subcontractors: $38,000 (low voltage, controls sub)

Subtotal Direct Costs: $284,000

Indirect Costs:

- Project management (25% of PM’s time allocated to this job): $8,500

- Safety compliance and training: $2,200

- Shop fabrication overhead: $4,800

Subtotal Indirect Costs: $15,500

Overhead Allocation: Using direct labor dollars as allocation basis (company overhead is 12% of direct labor):

- Overhead: $145,000 × 12% = $17,400

Total Job Cost: $284,000 + $15,500 + $17,400 = $316,900

If this was a $385,000 fixed-price contract:

- Gross Profit = $385,000 – $316,900 = $68,100

- Gross Margin = $68,100 / $385,000 = 17.7%

After company operating expenses, net margin might run 6-8%.

Understanding the variance: If your original budget was $295,000 total cost, actual came in at $316,900 – a variance of $21,900 (7.4%).

Job costing shows where that variance occurred:

- Labor hours: 1,850 actual vs. 1,680 budgeted (10% over)

- Material costs: $89,000 actual vs. $82,000 budgeted (8.5% over)

- Equipment: on budget

- Subs: on budget

The variance appears in labor hours and material costs. Investigation reveals the crew encountered unanticipated conduit routing challenges (affecting labor hours) and had to order upgraded panel components mid-project (affecting material costs).

This data informs your estimating database for similar future work.

Construction Job Costing FAQs

How to figure labor cost in construction?

Labor cost = (Total Hours × Burdened Hourly Rate)

The burdened hourly rate includes:

- Base wage

- Payroll taxes (FICA, Medicare, unemployment)

- Workers compensation insurance

- Benefits (health insurance, retirement, PTO)

- Other labor-related costs

For a worker earning $30/hour base wage, the burdened rate might run $42-45/hour when you include all burden costs for that construction job.

Multiply by actual hours worked on that specific project to calculate project labor expenses.

For detailed calculations including burden rate formulas, worker classifications, and prevailing wage tracking, see our complete guide on construction labor cost tracking.

What is the formula for job costing?

Total Job Cost = Direct L + Direct M + Direct E + Direct S + Indirect Costs + Overhead Allocation

Where:

- L = Labor

- M = Materials

- E = Equipment

- S = Subcontractors

This gives you fully burdened job cost including all direct work, indirect support, and overhead allocation.

To calculate profit: Profit = Contract Price – Total Job Cost

To calculate margin: Margin % = (Profit / Contract Price) × 100

Why is accurate job costing essential for construction companies?

Accurate job costing supports margin protection and helps improve job costing on future projects.

Construction net profit margins typically average around 5% – according to industry research, some regions run as low as 3.5%. When one particular job runs significantly over budget, it can offset profit from multiple successful projects and affect overall financial health.

Job costing systems that provide earlier visibility into cost variance – detecting issues at 5% over budget rather than 25% over – provide more opportunities to address problems during the active project phase rather than discovering losses after completion.

Additionally, every completed job adds actual cost data to your estimating intelligence for future projects. Contractors who maintain detailed job cost tracking build estimates based on documented performance rather than projection. This data-informed approach supports both bid competitiveness and margin consistency – essential for any successful construction business.

Fix the Foundation First

We’ve covered the complete job costing framework: cost categories, project budget comparison, variance analysis, contract-specific approaches, and best practices to improve job costing.

Construction companies implementing sophisticated job costing systems often discover a consistent pattern:

The system performs based on the data feeding it.

Your construction accounting software can calculate job costs with precision. Your cost codes can be organized systematically. Your variance reports can be automated to track progress. The reliability of these outputs depends on the reliability of your labor data – typically your largest cost category. When labor data comes from timesheets reconstructed from memory days later, that variance flows through every downstream calculation and affects your ability to manage costs effectively.

The SmartBarrel approach:

We don’t replace your accounting software or reinvent job costing methodology. We address the data capture foundation: labor data captured at the source rather than reconstructed later – giving you real time visibility into actual hours worked.

Workers check themselves in and out using biometric facial verification. Hours flow to your dashboard as they’re captured. Foremen or superintendents assign cost codes to pre-populated, facially verified timesheets rather than creating entries from memory. This eliminates the manual entry and transcription steps where variance typically enters job costing systems.

Your construction job costing software receives labor data captured at the source rather than reconstructed later.

The operational impact:

That variance analysis showing labor 15% over the project budget on a particular job? The data supporting it was captured at the source rather than reconstructed from memory.

That T&M invoice for 640 labor hours on that particular project? You have timestamped, geo-verified, biometrically verified documentation that addresses GC questions directly – protecting the project’s financial health.

That estimating database you’re building for future projects? It’s grounded in documented productivity data from completed projects rather than estimated costs based on assumptions.

Job costing reveals profit or loss on construction projects. Accurate labor data determines the reliability of what you’re seeing across the project lifecycle – essential for overall financial health and resource allocation for any successful construction business.

Construction Job Costing: FAQs

What is the difference between job costing and general accounting?

Job costing breaks down costs at the project level, tracking labor, materials, equipment, and indirects for each specific job. General accounting aggregates finances at the business level without that project-specific detail. Job costing provides granular insight that supports pricing and profitability decisions.

How often should job costing be updated during a project?

Job costing should be updated as frequently as possible, ideally daily or weekly, to reflect actual labor, materials, and equipment usage. Frequent updates allow managers to spot overruns early and adjust plans before costs escalate. Infrequent updates reduce the accuracy of forecasts and decision making.

How do indirect costs factor into job costing?

Indirect costs such as project management, office overhead, and support staff are allocated to jobs based on consistent drivers like labor hours or total costs. Including indirect costs ensures that all expenses supporting the project are captured, not just direct costs. Failing to allocate indirects underestimates true job costs.

How can job costing help control material waste?

By comparing planned material quantities and costs against what is actually used and invoiced, job costing highlights waste, theft, or ordering inefficiencies. This visibility helps teams refine purchasing, storage, and usage practices. Reducing waste directly improves margins.

What are common job costing mistakes to avoid?

Common mistakes include late or infrequent cost updates, not capturing indirect costs, misallocating equipment charges, and ignoring change order impacts. These errors lead to distorted cost visibility and poor decision making. Discipline in data capture and allocation prevents these pitfalls.